Lending FAQ

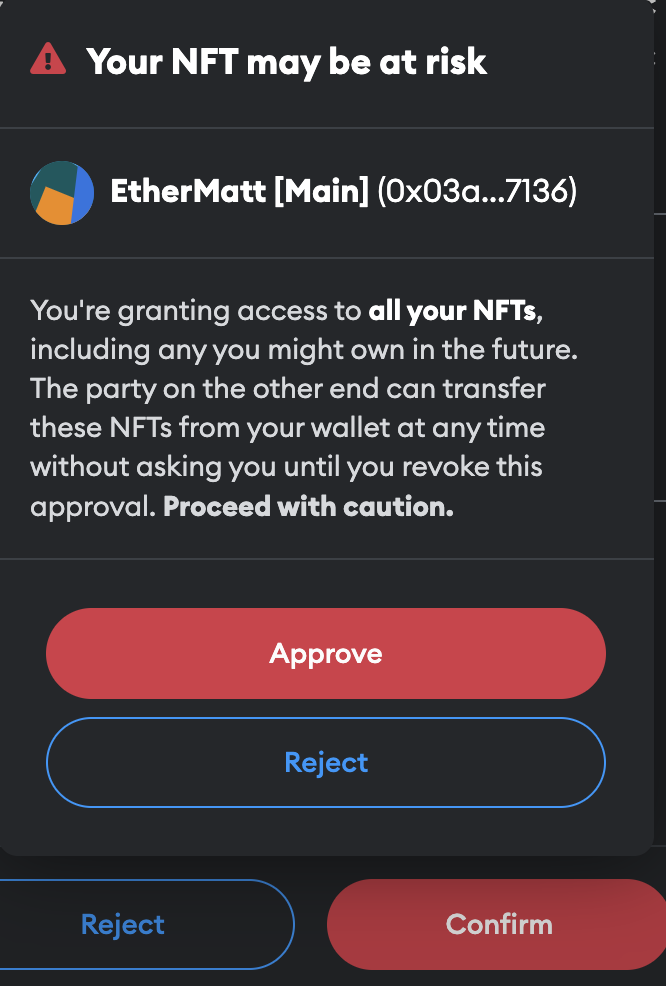

Why is Timeswap asking for NFTs approval? Is it safe?

Approving the request as shown in the above screenshot only allows the Timeswap smart contract to access the Timeswap (position) collection; it does not grant access to any of your other NFT collections.

In order to close your loan position, the Timeswap smart contract has to access the active NFTs.

Additionally, you could revoke access to the request using revoke.cash upon closing the loan positions.

Can I use my Timeswap lending position as collateral to borrow against?

No, your Timeswap lending position cannot be used as collateral in Timeswap, as your lending position is represented by an ERC-1155 token (and Timeswap only supports ERC-20 and ERC-4626 tokens).

What is the transition price?

Transition price (a.k.a. strike price) is the price point at and beyond which borrowers are expected to default, and the pool (asset) flips.

For example, an ETH-USDC pool in which users are using ETH as collateral.

When at maturity, market (spot) price > transition price, borrowers will ideally repay their USDC debt (and lenders will receive their USDC principal and interest).

Otherwise, borrowers will usually default on their USDC debt and forgo their ETH collateral (lenders will then receive ETH)

What does maturity mean?

As a lender, maturity indicates the time at which you will realise your principal along with the full interest.

What happens if I withdraw my lend positions before maturity?

Lenders that withdraw early (before maturity) will not receive the full interest. More details in the Deep Dive section.

Lenders that withdraw after maturity will receive full interest payment provided all borrowers repaid their debt.

Is the APR fixed once I open a lending position?

Yes, the APR you see on the UI is locked-in upon opening a lend/debt position. There will be no changes to your loan term’s parameters until the pool’s maturity time is reached (the APR you see on the UI -- after opening your position -- reflects the APR for a new lender/borrower).

Where is the yield coming from?

We are a lending/borrowing protocol, as such, the displayed APR is derived from interest payments.

Lenders’ interest payments come from the borrowers who pay interest to borrow against their collateral with no liquidations. In the case that there is a shortfall of borrowing demand, liquidity providers (LP) are the ones paying interest.

How is the collateral distributed to lenders when a borrower defaults?

Lenders will receive the equivalent amount of the forfeited collateral to their locked-in CDP (insurance amount).

For example, a lender lending 1,000 USDC to a USDC-ETH pool at a transition price of 1,000 and CDP of 150%.

This translates to 1.5 ETH as insurance to the lender.

When the market (spot) price < transition price (e.g., ETH trading at 800 USDC), borrowers are expected to default at maturity. The lender then receives 1.5 ETH (i.e., 1,200 USDC) upon maturity given that ETH took a 20% hit relative to the transition price.

Why are there different approvals for opening and closing a lend position?

When opening a lend position, the approval is for your ERC-20 asset to be lent to the pool.

When closing a lend position, the approval is for your ERC-1155 token (Bond Token) that represents your receipt for lending to the pool, the Bond Token will be burnt when closing your lending position.

Last updated